Scott Morrison’s third budget is headlined by $140 billion in tax cuts over the next decade, immediate tax relief of up to $1,060 a year for middle-income households and a fundamental reform of the tax system.

This Budget will be the last before the next federal election (due by May 2019) and not surprisingly, the proposals include a range of pre-election sweeteners. However, Treasurer Scott Morrison is also keeping the focus on a return to a surplus. Thanks to an improvement in the budget position of around $7bn per annum, the path to surplus has been made relatively easy for the Turnbull Government.

The modest fiscal stimulus will help households, but the main risk is that the revenue boost seen this year is not sustained and the budget continues to have relatively optimistic assumptions regarding revenue growth.

The Government’s stronger corporate revenue has mainly come from reduced tax losses and higher commodity prices. Added to this is stronger personal tax revenue thanks to higher employment and reduced spending. As a result, the 2017-2018 budget deficit is projected to come in at $18.2bn compared to $23.6bn in the Mid-Year review. Impact on the Reserve Bank of Australia’s interest rate settings and the share market is likely to be minimal, if at all.

Positive outlook

The Government has assumed that much of this revenue boost will continue (see the ‘Parameter changes’ line in the table below) and has only used a small part of it to fund tax cuts and other measures. The net result is that the budget is projected to continue to track to a surplus. This is now expected to be reached one year earlier in 2019-2020 albeit only just at $2.2bn in the positive or 0.1% of GDP. The move back to surplus is slowed slightly by the fiscal easing from policy changes, which are predominately tax cuts. For example, the 2018-2019 deficit is projected to fall to $14.5bn but it would have fallen to $13.8bn were it not for the tax cuts announced.

The planned tax cuts for higher income earners over the next decade are designed to satisfy the Government’s commitment from the 2014 Budget to cap tax revenue at 23.9% of GDP (or total revenue once dividends are allowed for as shown in the chart below at 25.4% of GDP). This is on the basis of the historic highs reached in the Howard resources boom years, and this cap is now projected to be reached in 2021-2022.

What’s next

The 2018-19 Budget has a sensible focus on providing a small boost to households (with the full impact of tax cuts not occurring until next decade) and to infrastructure at the same time as maintaining a return to surplus. The main risks are around whether the recent revenue windfall to the budget proves temporary and the assumptions for continued strong revenue growth.

If you would like to discuss the implications of any of the 2018 Federal Budget announcements to your personal situation, please contact Fintech Financial Services on telephone 07 3252 7665.

Summary of key Budget measures

Note: These changes are proposals only and may or may not be made law.

From 1 July 2018

- Low and middle income earners are to benefit from tax savings of up to $530 per person (or $1,060 per couple). This is mainly achieved by lifting the Low Income Tax Offset and raising the $87,000 tax threshold to $90,000.

- Dropping the planned 0.5% Medicare Levy increase, which will remain at 2%.

- The $20,000 instant asset write-off for business with aggregate turnover less than $10m will be extended until 30 June 2019.

- Funding for home care services and residential aged care will increase, and new products listed on the Pharmaceutical Benefits Scheme.

From 1 July 2019

- A one year exemption from the ‘work test’ will apply to recent retirees who have less than $300,000 in total super savings.

- Life insurance can only be offered in super on an ‘opt-in basis’ to new members under 25 years of age or members with inactive accounts or an account balance under $6,000.

- Fees when exiting a super fund will be banned and administration/investment fees will be capped at 3% pa on accounts with balances of less than $6,000.

- The ATO will work to proactively reunite Australians’ dormant superannuation funds with their active account, with inactive balances less than $6,000 to be transferred to the ATO.

- The Pension Loans Scheme will be available to all Australians over Age Pension age and the maximum payments will increase to 150% of the full Age Pension.

- An extra $25bn in infrastructure spending including the Melbourne rail link, Bruce Highway, Gold Coast/Brisbane M1, road and rail in WA and North-South Corridor in SA. This is only partly offset by various savings including an illicit tobacco tax and the usual tax integrity measures to target the black economy and multinational tax avoidance.

- Ongoing commitment to cut the corporate tax rate to 25% for large companies by 2026-27.

Opportunities post 1 July 2018

There are some key financial strategy opportunities for our clients following announcements made in previous Federal Budgets that are already legislated to take effect on 1 July 2018. These include:

- People aged 65 or over can make ‘downsizer’ super contributions of up to $300,000 from the proceeds of selling their home.

- First home buyers who have made super contributions under the First Home Super Saver Scheme can access their money for eligible property purchases.

- Where the annual concessional contribution cap is not fully utilised, it may be possible to accrue unused amounts for use in subsequent financial years.

Further information on these opportunities can found at the end of this summary.

Taxation

Personal income tax savings

Date of effect: From 1 July 2018

Low and middle income earners will benefit from initial tax savings of up to $530 per person (or $1,060 per couple) in the 2018-2019 financial year, then via a series of further tax cuts to be implemented over seven years.

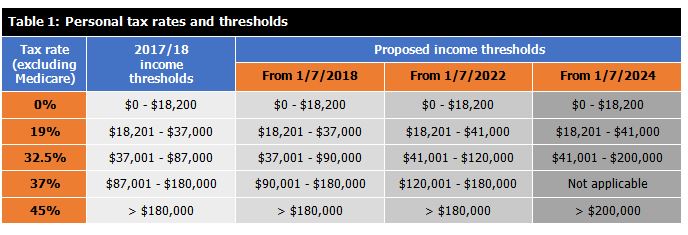

Personal income tax thresholds

Treasurer, Scott Morrison has a plan to fundamentally reform the tax system with changes to the income thresholds in 2022, and in 2024. The tables below show the impact of removing the 37% tax bracket and having the 32.5% tax bracket go all the way up to $200,000 on 1 July 2024.

Personal tax offsets

- A Low and Middle Income Earners Tax Offset of up to $530 will apply from 1 July 2018 to 30 June 2022.

- From 1 July 2022, the Low Income Tax Offset will increase from $445 to $645.

Personal tax savings

Table 2 below illustrates the tax payable in future financial years (and the potential tax savings compared to 2017/2018) for a range of taxable incomes. These figures take into account the proposed personal income threshold and tax offset changes.

Medicare levy to stay at 2%

The previously proposed increase in the Medicare levy to 2.5% from 1 July 2019 has been abandoned.

Extension of instant asset write off

Date of effect: From 1 July 2018

Small businesses with turnover of less than $10 million will be able to immediately write-off newly acquired eligible assets valued at less than $20,000 for a further 12 months.

Superannuation

Work test exemption for retirees

Date of effect: 1 July 2019

A person aged 65 to 74 is currently able to make contributions to superannuation if the ‘work test’ has been satisfied (i.e. they have worked at least 40 hours in 30 consecutive days) in the financial year the contribution is made.

A one year exemption from the work test will apply to older Australians who have less than $300,000 in total super savings. This exemption will apply to the financial year following the last year the work test was satisfied. This will allow an additional period of time for those eligible to contribute to superannuation.

Insurance in super

Date of effect: 1 July 2019

In many super funds, including MySuper and employer funds, insurance is offered as a default option. It’s proposed that members will need to ‘opt-in’ for insurance where they:

- have a balance less than $6,000

- are new members under age 25, or

- have an account which has not received a contribution in 13 months and are considered inactive.

Protection for small super balances

Date of effect: 1 July 2019

Measures will be introduced to reduce the impact of fees on low super balances and focus on returning lost super to members.

- Protection will be provided to super accounts by limiting administration and investment fees to a 3% annual cap. This cap will apply to accounts with balances below $6,000.

- Exit fees will also be banned on all super accounts.

- A $6,000 threshold will apply to inactive accounts. These accounts will need to be transferred to the ATO. The ATO will increase data matching activities to return amounts to active accounts held by members.

Personal deductions

Date of effect: 1 July 2018

The ATO will develop new compliance processes for taxpayers claiming a deduction for personal superannuation contributions. This includes raising awareness regarding the necessary steps, including lodging a ‘notice of intent to claim a tax deduction’ form with the super fund trustee.

Inadvertent concessional cap breaches

Date of effect: 1 July 2018

Employers are required to pay Superannuation Guarantee (SG) based on an individual employee’s income. For some individuals this means their concessional contribution cap is breached by the total of multiple employers’ compulsory contributions.

Individuals who have a total income exceeding $263,157 pa and multiple employers will have the option to elect to no longer have SG contributions paid on certain income from their employer. This overcomes the inadvertent breach of the concessional contribution cap and associated tax penalties.

SMSF increase in member numbers

Date of effect: 1 July 2019

Self-managed superannuation funds (SMSFs) are limited to having four members. This threshold will increase to six to provide greater flexibility and allow families, for example, to all be members of the same SMSF.

SMSF three-year audit cycle

Date of effect: 1 July 2019

SMSFs with a history of good record-keeping and compliance will move from providing an audit on an annual basis to a three-yearly cycle. Eligible SMSFs will be those with a history of three consecutive years of clear audit reports and have lodged annual returns on time.

Social security

Pension Loans Scheme

Date of effect: 1 July 2019

The Pension Loans Scheme allows eligible individuals to access some of the equity in the home or other property via a Government loan, which is advanced in fortnightly instalments.

This scheme will be available to all Australians over Age Pension age and the maximum loan payments will increase to 150% of the full Age Pension. Eligibility will continue to limited by the value of the property used as loan security.

The following table summarises the payment ranges for singles and couples based on current rates, where the full pension and no pension is available.

Work Bonus

Date of effect: 1 July 2019

Under the Work Bonus, the first $300 per fortnight (currently $250) of employment income will not count when calculating Age Pension entitlements under the income test.

Self-employed retirees will be able to access the scheme for the first time.

A ‘personal exertion test’ will ensure the bonus only applies to income earned from paid work.

Any unused Work Bonus (up to a total of $7,800 pa) can continue to be accrued to reduce assessable employment income in a future period.

Means-testing of certain lifetime income streams

Date of effect: 1 July 2019

Favourable social security rules will be introduced to encourage the development and use of income products that will help retirees reduce the risk of outliving their savings.

Under the proposed rules, only 60% of the amount initially invested in these ‘lifetime income streams’ will be assessed under the assets test. This concession will apply until the account holder is 84 (or for a minimum of five years). After this time, only 30% will be assessed for the rest of the person’s life. Also, only 60% of the income payments will be assessed under the income test.

Means testing of Carers Allowance

Date of effect: To be confirmed by Government

As previously announced, the Carer Allowance and Carer Allowance (child) Health Care Card will be income tested. Households earning over $250,000 won’t be eligible. Both existing and new recipients of Carer Allowance will need to meet this income test.

Aged care

Additional funding for aged care

Date of effect: From 1 July 2018

Funding for home care services and residential aged care will increase, including:

- 14,000 new home care packages over four years

- 13,500 new residential aged care places, and

- grants for aged care facilities in rural, regional and remote areas.

Legislated super changes post 1 July 2018

Downsizer contributions

Individuals aged 65 or older may be able to make super contributions of up to $300,000 (or $600,000 per couple) from 1 July 2018 when selling their home.

These contributions, known as ‘downsizer contributions’ can be made without having to meet a ‘work test’ or ‘total super balance test’ and they don’t count towards the contribution caps. However, they must be made with 90 days of settlement and a tax deduction can’t be claimed.

The property must have been owned for at least 10 years and have been the main residence at some time during this period.

First home super saver scheme – access

First home buyers who have made super contributions under the First Home Super Saver Scheme (FHSSS) can access their money from 1 July 2018.

The FHSSS started on 1 July 2017 and allows eligible first home buyers to save a deposit in the concessionally taxed superannuation system. Contributions of up to $15,000 per year (and a total of $30,000) can be made and they count towards the relevant contribution cap.

An online estimator is available to explore the potential benefits of using the FHSSS.

Catch-up concessional contributions

Where the annual concessional contribution (CC) cap is not fully utilised from 1 July 2018, it may be possible to accrue unused amounts for use in subsequent financial years.

The CC cap is currently $25,000 pa1. Counted towards this limit are all employer contributions (including super guarantee and salary sacrifice), personal tax deductible contributions and certain other amounts.

Unused cap amounts can be accrued for up to five financial years. 2019/20 is the first financial year it will be possible to use carried forward amounts.

To be eligible, individuals cannot have a total super balance exceeding $500,000 on the previous 30 June.

This measure could help those with broken work patterns and competing financial commitments to better utilise the CC cap. It could also help to manage tax and get more money into super when selling assets that result in a capital gain.

This cap applies in FY 2017/2018 and 2018/2019. It may be indexed in future financial years.

If balancing all those risks to form a better forecast of how they’ll play out or affect markets seems like a tough job, we couldn’t agree more. Clearly it’s hard to predict these issues in isolation. But in reality, these issues interact and evolve, and people react to them along the way, thus multiplying complexity and making outcome predictions next to impossible. No investor can consistently know how today’s concerns might affect markets in the future. Some current examples of this are:

If balancing all those risks to form a better forecast of how they’ll play out or affect markets seems like a tough job, we couldn’t agree more. Clearly it’s hard to predict these issues in isolation. But in reality, these issues interact and evolve, and people react to them along the way, thus multiplying complexity and making outcome predictions next to impossible. No investor can consistently know how today’s concerns might affect markets in the future. Some current examples of this are: