The October 2022 Federal Budget

Balancing a revenue windfall, pre-election promises, structural spending demands & persistent inflation pressures

The Labor Government under Anthony Albanese has implemented its election policies and expects lower budget deficits in the next two years thanks to increased tax revenues from higher commodity prices and other savings.

However, future years are expected to bring significant deterioration to the economy as structural spending pressures, higher interest rates and lower productivity impact growth. As the Treasurer Jim Chalmers foreshadowed, this is largely a “bread and butter” budget with no changes to personal income tax rates. Any other significant reforms being planned by the Labor Government across income tax rates or superannuation were not addressed in this budget and if they are applicable could be announced in next year’s 2023 Federal Budget in May.

Observations

- Yet another revenue windfall from high commodity prices and the offsetting of new spending with the savings, has resulted in sharply lower budget deficits over the next 2 years (the deficit this year has been revised down to $36.9bn from $78bn forecast in March 2022). This avoids adding to inflation and the pressure on the Reserve Bank of Australia (RBA) to keep raising interest rates.

- Budget deficit projections are now worse beyond 2024-2025 and will most likely lead to the Treasurer Jim Chalmers looking for was to increase fiscal (tax) revenues or cut spending in next May’s budget.

- There has been a realistic attempt to highlight the structural pressure on the budget whilst focussing on the cost of living pressures affecting less affluent Australians.

- The economic assumptions used in the budget look reasonable and Australia’s public debt remains low compared to other comparable countries, which will assist the Government retain its triple A credit rating.

- Commodity price assumptions used in the budget remain well below current levels and so could be a source of surprise to reduce the deficit further.

Key proposals

- Reducing eligibility age for Downsizer Contributions from 60 to 55.

- Increasing Commonwealth Seniors Health Card income thresholds.

- Allowing pension age social security recipients to earn more from employment before their payment is impacted.

- More generous eligibility rules for Child Care Subsidy and Parental Leave Pay.

- More favourable Centrelink assessment of home sale proceeds.

- Continued support for homebuyers, and

- Increased funding for the National Disability Insurance Scheme (NDIS).

Please note: The announced changes are proposals only and may or may not be made law.

The successful implementation of the measures will require successful negotiation through the Senate where the Government does not hold a majority. Therefore, The final version of these measures may differ from the current announcements.

Summary

Personal Taxation

- No changes to personal income tax: The Budget did not contain any measures announcing changes to personal income tax. This includes:

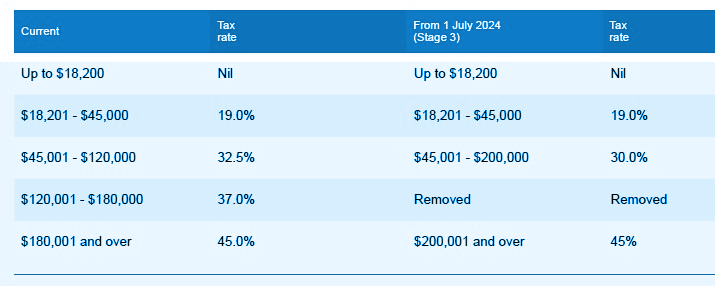

- No changes to the Stage 3 tax cuts (announced by the former Liberal Government) which are still tabled to take effect from 1 July 2024, and

- No extension of the Low and Middle Income Tax Offset, which ended 30 June 2022.

- Helping enable electric car purchases: For purchases of battery, hydrogen, or plug-in hybrid cars with a retail price below $84,619 (the luxury car tax threshold for fuel efficient vehicles) after 1 July 2022, fringe benefits tax and import tariffs will not apply. Note: Employers will still need to account for the cost in an employee’s reportable fringe benefits.

No changes to personal tax rates and thresholds

Home Ownership

- Housing affordability measures: A key focus of the Budget were measures to help individuals secure housing. This is expected to occur largely via the Housing Accord – which will bring Federal, State and Local Governments together to work on housing affordability and homelessness. Measures announced include:

- A commitment to the ‘Help to Buy’ scheme which will support first home buyers to buy a home with the Federal Government being a part owner, resulting in a lower balance to be funded by the individual themselves.

- A Regional First Home Buyer Guarantee from 1 October 2022 which, similar to the existing First Home Deposit Guarantee scheme, is expected to provide up to 10,000 first home buyers with a guarantee over their mortgage, removing the need for lenders mortgage insurance

Superannuation

- Expanding eligibility for the Downsizer Contribution: Legislation has been introduced to reduce the Downsizer Contribution eligibility age from 60 to 55 years of age. This measure will allow more people to make a further contributions of up to $300,000 each to their Superannuation after selling their family home owned for more than 10 years. The measure is proposed to take effect from the first quarter after passing into law, which is expected to be 1 January 2023.

- SMSF and tax residency: The Government confirmed its intention to continue with the 2021/22 Budget measure of extending the temporary trustee absence period from two years to five years and removing the ‘active member’ test. These changes will help SMSFs continue to maintain their Australian tax residency even while members are overseas, and allow them to continue to contribute to their funds even if they become non-tax residents.

- Three-year audit cycle for SMSFs not proceeding: Originally announced as part of the 2018/19 Budget, it was confirmed the current Government will not proceed with this measure.

Social Security

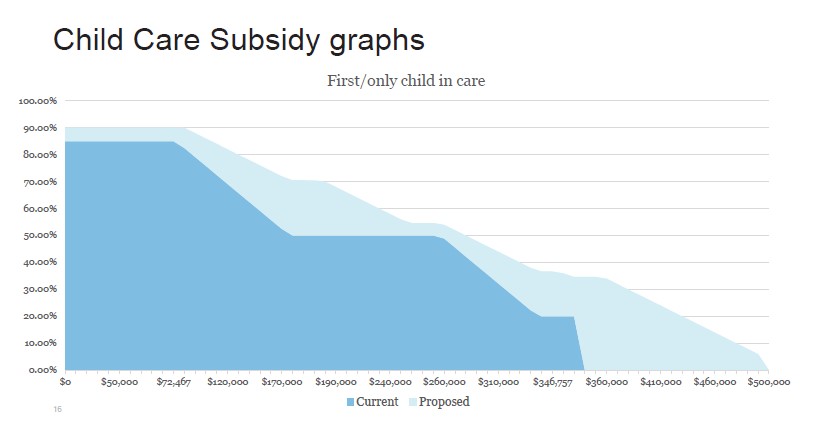

- Child care subsidy changes: As part of a package of reforms to encourage parents to return to the workforce, the maximum child care subsidy from 1 July 2023 will increase to 90% for families earning less than $80,000. For every $5,000 earned over this threshold the subsidy will reduce by 1% – reducing to zero for incomes $530,000 or above. The higher rate of subsidy for families with multiple children in care will continue under its current arrangements, ceasing once the eldest child reaches six years old or has been out of care for 26 weeks.

- Paid parental leave increases: Announced before the Budget, from 1 July 2024 the Paid Parental Leave Scheme will increase the maximum period of leave by two weeks each year – reaching a maximum of 26 weeks by 1 July 2026. Further, from 1 July 2023 both parents will be able to access leave at the same time or enter into more flexible arrangements than currently available under the limited Dad and Partner Pay limits, and requirements to take 12 weeks as a continuous period. The paid parental leave income test will also be extended to include a $350,000 family income test, which can be used to help families who do not meet the individual income test.

- Reducing assessment of former home proceeds: For individuals on social security benefits, the temporary assets test exemption of home sale proceeds is to be extended from 12 months to 24 months. Additionally, these proceeds will only be deemed to earn a return at the lower deeming rate (currently 0.25% per annum) for this period. Note: This exemption only applies to the portion of the proceeds expected to be used in a new home purchase.

- Work Bonus deposit for older Australians: Announced as an outcome from the Jobs and Skills Summit, age pensioners and veterans over service pension age are expected to receive a one-off credit of $4,000 into their Work Bonus income bank. The Work Bonus typically offsets $300 per fortnight of income earned from employment or self-employment activities, allowing pensioners to receive a higher age pension whilst still working.

- Increased income thresholds for Commonwealth Seniors Health Card: The Government has committed to increasing the income thresholds to qualify for the Commonwealth Seniors Health Card from $61,284 to $90,000 for singles, and from $98,054 to $144,000 combined for couples. This measure creates an opportunity for more senior Australians to access reduced costs for healthcare, pharmaceuticals, utilities and transport and more.

- Deeming rate freeze: The Government has also confirmed its intention to retain the current deeming rates until at least 30 June 2024.

- Plan for cheaper medicines: From 1 January 2023, the general patient co-payment for Pharmaceutical Benefits Scheme treatments is expected to reduce from $42.50 to $30.

Implications for asset classes and investments in Australia

- Cash and term deposits: Returns on Cash accounts are improving thanks to the current RBA interest rate hikes but still remain historically low. Term Deposits rates being paid by some banks for longer terms such as 12 Months, are becoming more attractive at 3.8% and higher levels.

- Bonds: The RBA has hiked interest rates rapidly from 0.10% to 2.60% since April 2022, and are widely expected to increase rates further in November and December 2022 by 0.25% or 0.50% before pausing early in early 2023.

- The need to keep increasing rates is due to persistently high inflation, full employment and overheating markets following the trillions of dollars of stimulus injected into the economy along with interest rate cuts following the breakout of the COVID-19 pandemic in early 2020.

- Further rate hikes and forecast budget deficits (albeit deficits may now be lower than expected) will continue to add upwards pressure to bond yields in the near term.

- Investors who purchased fixed rate and long duration bonds purchased before the recent interest rate increases have lost capital value in those bonds. In fact, bonds have dropped over -12% in the last 6-9 months. Bond markets are reaching the peak in this cycle and have now pricing in yields around 4% (compared to 0.20% 6 months ago).

- As the impacts of higher interest rates and other Government austerity measures are felt, inflation and the economy growth will start to show more signs of contraction. Current bonds yields at around 4% and higher are becoming attractive in anticipation of this, and we are positioned to take advantage of buying opportunities as they arise for your portfolio.

- Shares: The budget is positive for childcare and construction companies but beyond that there is not really a lot to impact the share market. However, we are continuing to focus on high quality Australian and International companies that have strong competitive positions in their markets, resilient earnings, positive cash flows and low levels of debt.

- Property: The confirmation of more homebuyer schemes and more immigrants offset by long term housing supply measures in the budget are unlikely to alter the dominant negative impact of rising mortgage rates in driving a cyclical downturn in home prices into 2023.

- The Australia Dollar (AUD): the Budget is unlikely to change the direction for the AUD, particularly against the strong USD as inflation remains high and the US Federal Reserve continues to hike interest rates.

The above budget initiatives have the potential to deliver benefits to you depending on your financial situation, personal circumstances and stage in life. Please contact us if you would like to discuss any of this further.

As usual, we are looking forward to continuing to assist you confirm the important financial strategy areas relevant to you and provide advice to maximise your outcomes in the long term future.

Leave a Reply

Want to join the discussion?Feel free to contribute!